The work of a commercial company is assessed by profit. But the numerical expression poorly reflects the dynamics by month, because revenue varies depending on the season and other factors. Therefore, the marginal profit indicator is often used as a percentage. We will look at how to calculate margin in detail in this article.

Margin concept

The term comes from the English “margin” translated as difference, advantage. The basic values are the cost of the product and the price for the end consumer. Marginal profit is expressed as a percentage, which reflects the dynamics of the enterprise's profitability, regardless of the size of operating costs and revenue received.

Rice. 1. A high profit margin does not always mean a high margin.

The concept of margin is applied regardless of the sphere: bank, production, provision of household services to the population. The generalized indicator, at first glance, is effective in different areas of accounting.

What types of margin are used?

Accounting for a small company where overall profit is key is one thing. Another case is when a manager needs to calculate the efficiency of different departments: purchasing, sales, production. Then you have to separate the financial results and calculate the margin based on “individual” indicators.

Margin is most often divided into categories:

- gross Sometimes they say “gross margin”. Suitable for calculating the level of costs for the purchase of raw materials, sales of goods, and payment of wages;

- operating room This is the ratio of operating profit to enterprise income. It indicates the efficiency of the work (the higher the better). In practice, this figure is used when assessing intermediate results to track dynamics in production/trade;

- clean. Profit per unit of revenue. This indicator is good for departments working on planning the company's future activities. It is used in large enterprises where the cost part of the budget can vary significantly;

- interest. Used by banks and other financial institutions. There are absolute and relative indicators. The first option shows how successful the company is in the current period, the second - in comparison with previous results.

How is margin calculated?

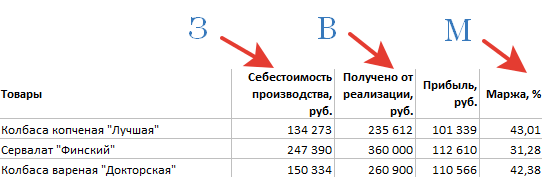

If desired, this can be done on a calculator, but tables are more convenient, because can become an appendix to a report; they can be used to create graphs and diagrams. The initial data is taken in rubles, the result of the calculations is obtained as a percentage.

Margin formula:

M = (H – W)/H x 100%, where

M – margin (in percent); B – gross revenue (of an enterprise or a separate division); C – costs (product cost, rent, salaries, taxes).

Rice. 2. A similar table is compiled at the end of each reporting period

The proposed marginality formula remains unchanged regardless of the source data. For example, the sales department takes the purchase price of goods, costs for warehouse space, transport, and salaries as indicator “Z”. In production, instead of goods, raw materials and consumables used in the manufacture of products are taken into account.

The given formula is entered into an Excel table, the required columns are indicated, and the source data is entered into the corresponding columns.

Comparison of individual periods (months, quarters, years) allows you to evaluate the dynamics and determine the general trend - whether there is a decline or rise. The larger the enterprise, the more often it is recommended to make such cuts.

Rice. 3. According to this graph, it is easy to see an increase in costs and a decrease in profits

Percentages are also used to calculate coefficients. This is a comparison of the profitability of purchasing individual batches of raw materials and working with suppliers. The formula for calculating margin is also in demand when creating a business plan for new directions. Thanks to the availability of figures on profit margins and cost amounts, it is easier to plan the development of the company (is there enough market potential, is it necessary to expand to other regions).

Are there differences in markup and margin calculations?

When preparing the initial data for calculating margin as a percentage, it is worth considering the difference between margin and markup. Often the second concept is used as a synonym for the term “profit”. But in practice its purpose is somewhat different.

Markup is an increase in the cost of goods/services when counterparties choose additional delivery conditions stipulated by the contract.

It turns out that the markup is only part of the margin. Most often, they resort to it if operating costs increase, new contractors have to be involved, equipment has to be purchased in order to fulfill the new terms of the contract. If you use the markup as the initial data and try to calculate the cost-effective level of costs from it, you will get an unreliable figure.

The value of margin analysis in business

Drawing up margin reports for the reporting period and comparing values for different months/years plays a significant role in making management decisions. The work of a number of departments (employees) is based on this indicator. Thanks to its accurate data, the following work is carried out:

- analysis of the results of the organization’s activities;

- management of fixed costs;

- determination of the critical level of operating expenses;

- calculation of break-even level and profitability in new areas.

The indicator is useful both for the enterprise and for analyzing individual groups or names of goods, identifying profitable types of products.

It happens that if you want to start doing a certain business, you lack knowledge in this area. First, let's look at the basic terms and their meanings. Many new entrepreneurs have no idea what margin is. This concept is broad and has different meanings in different areas of activity.

Margin is usually called the difference between the selling price of goods and their cost, quotes on stock exchanges and interest rates. This term is widely used in banking, trading and risk insurance. Each area has characteristic nuances. It can be calculated both in absolute values and as a percentage.

So what is margin in trading? In economic theory, this is the difference between two criteria for a product - price and . In this case, it is calculated using the following formula:

Margin = (product price - cost) / product price x 100%.

The indicators in the formula can be expressed both in rubles and in other absolute values (dollars, euros).

When analyzing the activities of an enterprise, the economist-analyst's main interest is the gross margin, which is calculated as the difference between the company's revenue from sales of products and additional costs. These also include variable costs, which are directly dependent on the volume of products produced. The size of the gross margin is directly proportional to the amount from which fixed development funds (capital) are formed.

It should be clarified that this concept in the Russian Federation differs from the meaning of the term in Europe. There, margin is understood as the percentage rate of the ratio of profit to sales of goods at the selling price. This value is used for a relative assessment of the effectiveness of the company’s economic and trading activities. In Russia, margin is usually called the net profit from a transaction, that is, income from sales minus the cost of goods and other costs.

Application of margin in banking

Let's consider a term in this area. The concept of credit margin is applicable here - the difference between the contractual cost of the goods and the actual amount that is issued to the borrower. All funds under the transaction are specified in the loan agreement. directly depends on the difference between interest rates on loans and deposits). Net interest margin is perfect for these purposes. It is calculated as the difference between the net interest income of a credit institution (obtained through investments and lending) and the rate on liabilities or capital.

When it comes to , the guarantee margin is used, the formula of which is calculated as the difference between the value of the pledged property or funds and the size of the loan.

Use in exchange activities

The use of variation margin on exchanges is primarily associated with futures trading. In this case, its name can be explained by constant fluctuations, or changes. The calculation is made from the moment the position is opened.

For example, we purchased a futures contract at a price of 150,000 points on the RTS index, and a few minutes later it increased to 150,100 points. In this case, the margin size is 150100 – 150000 = 100 points. When converting this parameter into rubles, you get approximately 67 rubles. If you do not take profit and keep the position open, at the end of the trading session (evening clearing) the variation margin will turn into accumulated income. On the next day of trading, its accrual will begin again.

In other words, if we kept the position open for the entire duration of one trading session, the profit or loss on the transaction will be equal to the margin. The position was not closed for several sessions - the result will be the sum of the margin values for each past day. In this case, we can conclude whether we have set the right direction. Profit on the selected time interval will confirm this. A negative value means that the trading account has suffered losses.

In other words, if we kept the position open for the entire duration of one trading session, the profit or loss on the transaction will be equal to the margin. The position was not closed for several sessions - the result will be the sum of the margin values for each past day. In this case, we can conclude whether we have set the right direction. Profit on the selected time interval will confirm this. A negative value means that the trading account has suffered losses.

The difference between margin and markup

Exchange margin is a specific concept, as it is used only in trading. Trading margin is the most common term in many industries. However, there are a lot of misconceptions among non-professionals. One of them is equating it to the trade margin.

It is not difficult to identify the difference between the two concepts. The margin indicator is the ratio of profit to the market price of the product. The markup is the ratio of the profit of a product to its cost.

The product was bought for 150 monetary units and sold for 200. Calculating the markup is very simple: (200-150)/150 = 0.333(3), that is, 33% of the cost of production.

We calculate the margin:

(200-150):200=0.25. It amounted to 25% of the market value of the goods.

What's the difference between margin and profit?

As mentioned earlier, this concept is different in Russia and the EU countries. We have already considered the European method of calculation. In the Russian Federation, margin is considered an analogue of net profit, so there is no difference in their calculations. However, it should be borne in mind that we are talking about profit, and not about trade margins.

It is important to know the differences between economic terms and indicators. The concept of margin is used to calculate the most important financial indicators. This is necessary when working with securities, in banking, and on stock exchanges. For a trader, the size of the margin provided by the broker plays a huge role. When analyzing sales profit, it is compared with retail margins.

In general, the term “margin”, which recently came to e-commerce, is used in stock exchange, trading, and banking practice. It denotes the difference between the selling price and the cost per unit of production. This is often referred to as the profit received per unit of production or the profitability ratio as a percentage of the selling price. Essentially, this is return on sales. And the profitability ratio is the main indicator that determines the profitability of the entire enterprise as a whole.

Basic calculation formulas

M = OC – SP, where:

M – margin (called profit per unit of production)

OTs – the value of the selling price,

SP is an indicator of the cost of production.

K = P / OTs, where:

K – the value of the profitability ratio in %,

P – profit per unit. products

Commercial meaning and significance of the concept of margin

The higher the ratio, the more profitable the company is. The success of a company is determined by its high margins. Any decision made by top managers in the field of marketing strategies should be based on margin analysis. A key factor in forecasting the profitability of potential clients, the profitability of marketing itself, and the formation of a pricing policy is also the margin.

About Product Units

Each company has its own unit value when calculating commercial margin. It can be expressed in tons, pieces, liters, etc. For example, the tobacco industry operates both in pieces of cigarettes and in blocks, packs, and boxes. In banking, margin is calculated based on the number of accounts, clients, transactions, loans, etc. For example, the margin in a bank may be the difference between rates on deposits and loans. In the stock market, the difference between the price of securities on the day of conclusion and the day of execution of the transaction. In marketing, this is a markup set by businesses. Instant switching from one conceptual calculation model to another is a necessary condition for the professional activities of managers.

The so-called gross profit existing in Russia is nothing more than marginal profit. Although it can still be called that with some stretch. Essentially, this is the difference between the profit from the sale of manufactured products (excluding VAT and excise taxes) and production costs. Another common name for contribution margin (MP) - coverage amount - more clearly defines it as the part of revenue that goes to generating profit and covering costs. The meaning of the indicator is that the higher the MP, the faster the cost recovery will occur and, accordingly, the higher the profit received by the enterprise.

Calculation

How to calculate the margin in this case? Without further ado, marginal profit is calculated per unit of manufactured and sold products. From this calculation it immediately becomes clear whether we should expect an increase in profit due to the release of each individual unit of goods. The calculated marginal profit indicator does not characterize the efficiency of the enterprise as a whole, but helps to identify the most profitable (and most unprofitable) types of products in terms of possible profitability. MP depends on such volatile market indicators as variable costs and price. To achieve an increase in marginal profit (income), you have to increase the markup on products and/or sell more. Marginal profit is the difference between sales income and variable costs.

Sometimes another name is used - contribution to the coverage. MP is a contribution to generating profit and covering costs (fixed). If an enterprise produces or sells several types of products, calculating marginal profit is simply necessary. It will allow you to calculate the share of contribution of each type to the total income of the enterprise. Based on the calculation results obtained, a group of more profitable products is selected and less profitable ones are eliminated.

Sometimes another name is used - contribution to the coverage. MP is a contribution to generating profit and covering costs (fixed). If an enterprise produces or sells several types of products, calculating marginal profit is simply necessary. It will allow you to calculate the share of contribution of each type to the total income of the enterprise. Based on the calculation results obtained, a group of more profitable products is selected and less profitable ones are eliminated.

The next indicator - the rate of marginal income - determines the share of marginal income in revenue after sales or the share of the average value of MP in the price of the product.

European accounting system

The European accounting system defines the concept of margin completely differently. If in Russia “margin” is rather synonymous with profit, then in Europe gross margin is an indicator of the total income from sales after direct costs incurred for the production of goods and services. It is expressed as a percentage.

Margin 100 – 200% - is this possible?

Sometimes in the press and in behind-the-scenes conversations one hears such victorious statements. But can this be true? Based on the very definition of margin - an indicator of profitability of sales - definitely not. Margins can approach 100% due to cost reduction. But just as there cannot be zero cost, there cannot be a margin (profitability) of 100%.

Margin is one of the determining factors in pricing. Meanwhile, not every aspiring entrepreneur can explain the meaning of this word. Let's try to rectify the situation.

The concept of “margin” is used by specialists from all spheres of the economy. This is, as a rule, a relative value, which is an indicator. In trade, insurance, and banking, margin has its own specifics.

How to calculate margin

Economists understand margin as the difference between a product and its selling price. It serves as a reflection of the effectiveness of business activities, that is, an indicator of how successfully the company converts into.

Margin is a relative value expressed as a percentage. The margin calculation formula is as follows:

Profit/Revenue*100 = Margin

Let's give a simple example. It is known that the enterprise margin is 25%. From this we can conclude that every ruble of revenue brings the company 25 kopecks of profit. The remaining 75 kopecks relate to expenses.

What is gross margin

When assessing the profitability of a company, analysts pay attention to gross margin - one of the main indicators of a company's performance. Gross margin is determined by subtracting the cost of manufacturing a product from the revenue from its sale.

Knowing only the size of the gross margin, one cannot draw conclusions about the financial condition of the enterprise or evaluate a specific aspect of its activities. But using this indicator you can calculate other, no less important ones. In addition, gross margin, being an analytical indicator, gives an idea of the company's efficiency. The formation of gross margin occurs through the production of goods or provision of services by the company's employees. It is based on work.

It is important to note that the formula for calculating gross margin takes into account income that does not result from the sale of goods or the provision of services. Non-operating income is the result of:

- writing off debts (receivables/creditors);

- measures to organize housing and communal services;

- provision of non-industrial services.

Once you know the gross margin, you can also know the net profit.

Gross margin also serves as the basis for the formation of development funds.

When talking about financial results, economists pay tribute to the profit margin, which is an indicator of the profitability of sales.

Profit Margin is the percentage of profit in the total capital or revenue of the enterprise.

Margin in banking

Analysis of the activities of banks and the sources of their profits involves the calculation of four margin options. Let's look at each of them:

- 1. Banking margin, that is, the difference between loan and deposit rates.

- 2. Credit margin, or the difference between the amount fixed in the contract and the amount actually issued to the client.

- 3. Guarantee margin– the difference between the value of the collateral and the amount of the loan issued.

- 4.

Net interest margin (NIM)– one of the main indicators of the success of a banking institution. To calculate it, use the following formula:

NIM = (Fees and Fees) / Assets

When calculating the net interest margin, all assets without exception can be taken into account or only those that are currently in use (generating income).

Margin and trading margin: what is the difference

Oddly enough, not everyone sees the difference between these concepts. Therefore, one is often replaced by another. To understand the differences between them once and for all, let’s remember the formula for calculating margin:

Profit/Revenue*100 = Margin

(Sales price – Cost)/Revenue*100 = Margin

As for the formula for calculating the markup, it looks like this:

(Selling price – Cost)/Cost*100 = Trade margin

For clarity, let's give a simple example. The product is purchased by the company for 200 rubles and sold for 250.

So, here is what the margin will be in this case: (250 – 200)/250*100 = 20%.

But what will be the trade margin: (250 – 200)/200*100 = 25%.

The concept of margin is closely related to profitability. In a broad sense, margin is the difference between what is received and what is given. However, margin is not the only parameter used to determine efficiency. By calculating the margin, you can find out other important indicators of the enterprise’s economic activity.

The concept of marginal profit (MR, marginal revenue) is complex and includes 2 parts, and theorists and practitioners attach different meanings to each of them.

Word " margin"came to us from the English language, in which, from the point of view of the market concept, it denoted the difference between the price and the cost of a product; now it is widely used in the trading sphere, by stockbrokers, bankers and insurers to denote the difference between the values of various indicators.

The domestic concept of “Profit” has a similar content and is defined as the difference between the total income and expenses of the organization. In practice, accounting and economic are usually distinguished.

Since in the Russian Federation accounting, management and tax accounting have long become separate types of accounting due to legislative quirks, the meaning of the above definitions must be approached taking into account the goals that business owners and managers want to achieve.

Marginal profit(the amount of coverage, marginal or marginal income) is usually called the result - revenue from sales of products minus variable costs.

In Russia, in fact, the terms margin and marginal profit are used as equivalent. As a difference, we can point out that the concept of margin is more actively used in trading, where it is often used as an analogue of trade margin, which is not true.

When communicating with other specialists, always clarify the meaning that they attach to certain words.

The commercial meaning of contribution margin

Whatever options scientists offer as the main essence for assessing the efficiency of companies, in simple language, the goal of any business activity is net income, and all other calculated values are derived from it.

After all, if a business does not exist, then sooner or later it will cease to exist.

The amount of coverage is one of the most important indicators for analyzing the profitability of an organization and is necessary for making the right management decisions. See fig. 1.

Rice. 1. Indicators describing profitability;

The size of the MR indicator is always the largest of all that characterize profitability; the others are smaller than it, respectively, by the amounts of fixed costs, non-operating expenses, income tax and payments from it.

For a deeper understanding of what marginal income is, it is necessary to clearly understand what components it consists of. In particular, at the top level these are sales revenue, general variable and fixed costs.

Thus, the coverage amount is understood as that part of the incoming cash flow, due to which profit is generated and the company’s fixed expenses are covered.

The calculation of this indicator by type of product allows us to identify the dependence of the total added value on the contribution of each of them, making explicit the connection between the increase in profitability and the production and sale of an additional copy of the product, which is ultimately necessary for top management or the owner to develop and make informed management decisions in areas of marketing and production.

There are only two main ways to increase MR:

- An increase in the price of a product and/or its sales volume. A move in this direction usually encounters obvious market restrictions;

- Reducing costs and, above all, variables.

Since MR is most often understood as the difference between the gross income from the sale of a unit of goods and the variable costs for it, the formula for calculating the margin will look like this:

In practice, it can be calculated in both absolute and relative terms.

Calculation of marginal profit formula

It is believed that the larger the MR value, the better, since the organization must not only cover its fixed costs, but also receive significant benefits.

Most often, the formula for calculating marginal profit is as follows:

MD = VD-PI, where

MD - marginal income;

VD - gross income;

PI - variable costs.

It is important to take into account that when determining the amount of revenue for the correct calculation of the MD, indirect taxes are excluded from it, now these are VAT, excise taxes, etc.

Disadvantages of the marginal analysis method

- The assumption that the release of one additional piece of goods does not affect fixed costs, although from the standpoint of simple common sense it is obvious that personnel will have to work more and equipment will wear out faster, and, therefore, depreciation should be accelerated, which, within the framework of marginal analysis, refers to him;

- Variable costs for the production of a product on the part of the enterprise, from the point of view of the cost of producing a unit of production, become constant;

- Assumption of the invariability of influencing factors, such as technology, labor productivity, scale of production, etc.;

- Assumption that the relationship between MD and costs is linear;

- Acceptance of the hypothesis that everything produced will be sold at the same price.

To summarize, it must be said that in order to accurately calculate the amount of coverage within the company, high-quality and operational management accounting must be properly established, and the above-mentioned disadvantages of the marginal approach must be taken into account.